Blog: finance and real estate made simple

Articles and insights to help you navigate and grow

30 Years of Mortgages in the Czech Republic: Hindsight Is 20/20 — But What Can We Learn?

“If I had known back then what I know today, I would have bought several apartments.”

We hear similar statements quite often these days. But hindsight is always 20/20. Instead of speculating, let’s look at hard data from the past thirty years of the Czech mortgage market.

Let’s focus on four key indicators:

- average apartment price

- average wage

- average mortgage size

- mortgage interest rates

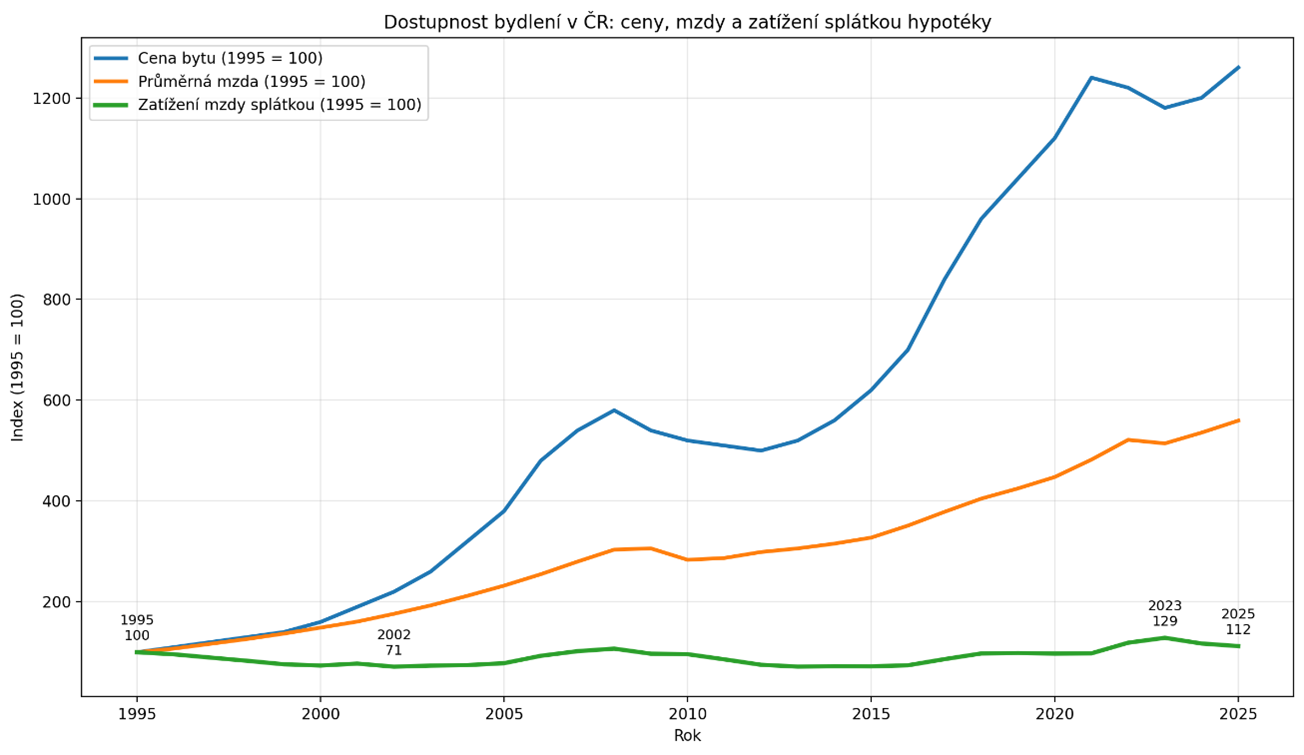

How property prices have grown

In 1995, the average apartment cost was approximately CZK 500,000. By 2025, it is around CZK 6,300,000. That means prices have increased roughly 12.6 times. In long-term terms, this represents an average annual growth of about 8.7%.

Property prices have therefore risen significantly over the past three decades and have become one of the most important household assets.

How mortgages have grown

As property prices increased, mortgage sizes naturally followed.

In the mid-1990s, the average mortgage was around CZK 400,000.

Today, a typical mortgage is about CZK 4 million. That’s roughly a tenfold increase. At the same time, the absolute amount of equity buyers need has also risen significantly.

How wages have grown

Income development provides important context. In 1995, the average monthly wage was about CZK 8,400. Today, it is roughly CZK 47,000 — an increase of about five times.

At first glance, it may seem that rising property prices are offset by rising wages. The reality, however, is more complex.

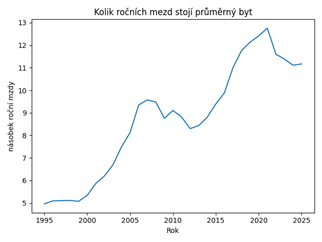

Housing affordability

If we compare apartment prices to annual household income, we get a more telling picture.

In 1995, an average apartment cost about 5 years’ worth of wages. Today, it costs roughly 11 years’ worth.

In other words, housing is now about twice as unaffordable as it was thirty years ago when measured against income.

Interest rate trends

We often hear that mortgages are expensive today. History, however, paints a slightly different picture.

In 1995, the average mortgage rate was around 13%.

In 2025, it ranges between approximately 4.19% and 4.99%.

Over the past thirty years, the average mortgage rate has been around 5%.

Interest rates fluctuate, but in recent years they have remained within a relatively stable range.

Key takeaways from the past 30 years

The paradox of 1995:

Although apartments were “cheap,” mortgages were extremely expensive and wages were low. Monthly payments consumed over 50% of income — very similar to today.

The golden era (around 2015):

A combination of reasonable prices and record-low interest rates reduced the mortgage burden to a historic low (around 34% of income). This was the period of highest affordability.

Today’s reality (2025):

We are at a point where the gap between wage growth and property prices is the widest in history. Despite lower interest rates than in the 1990s, housing is now the least affordable in the past 30 years, as the average mortgage payment takes the largest share of the average salary (around 55%).

What history shows us

The history of the Czech mortgage market highlights several important points:

- Real estate tends to appreciate over the long term. Over the past thirty years, the average apartment price has increased more than twelvefold.

- Interest rates are not the main factor. Rates change over time, but their impact on long-term housing decisions is often overestimated.

- The biggest risk is waiting. History shows that people rarely regret buying property too early. More often, they regret not buying sooner. That’s why it makes sense to rely not only on emotions, but primarily on data.

Hindsight is always 20/20. What matters is how you decide today.

Whether you’re just considering buying a home or already planning a specific step, you don’t have to go through it alone. We’re happy to walk you through your options, explain the context, and help you find a solution that is sustainable in the long run.

Sources: Kurzy.cz, Hypoindex, Czech National Bank, Czech Statistical Office.

Kalkulačka

Calculate

-

Monthly installment

Next step with Stone & belter

Stone & belter blog

Similar articles

Category

10.06.2026

Mortgage Fixed Rate Expiring? Don’t Accept the First Offer from Your Bank Without Checking Your Options.

Ondřej Marek

21.04.2026

30 Years of Mortgages in the Czech Republic: Hindsight Is 20/20 — But What Can We Learn?

12.03.2026

Investment Mortgages to Face Stricter Rules: What Will the New Regulation Bring in 2026?

Ing. Lukáš Cinko

11.06.2025

Understanding the Mortgage Process for Foreigners in the Czech Republic – Part 2

Mgr. Petra Šichová

10.02.2025

Czech National Bank Cuts Interest Rates to 3.75%: What This Means for Your Savings, Mortgages, and Investments

Ondřej Marek

29.09.2024

Mortgages and Interest Rates: Why Are They More Expensive Than Everyone Expected?

Ondřej Marek

28.05.2024

Early Mortgage Repayment Will Get More Expensive – Limiting “Mortgage Tourism”

Ing. Lukáš Cinko

16.04.2024

Options for Reducing Your Mortgage Interest Rate During the Fixed Period

Ing. Alena Lodlová07.12.2023

Major Updates and Changes in 2024 in Building Savings, Mortgages, Insurance, and Pension Savings

Ondřej Marek10.06.2026

Mortgage Fixed Rate Expiring? Don’t Accept the First Offer from Your Bank Without Checking Your Options.

Ondřej Marek21.04.2026

30 Years of Mortgages in the Czech Republic: Hindsight Is 20/20 — But What Can We Learn?

12.03.2026

Investment Mortgages to Face Stricter Rules: What Will the New Regulation Bring in 2026?

Ing. Lukáš Cinko11.06.2025

Understanding the Mortgage Process for Foreigners in the Czech Republic – Part 2

Mgr. Petra Šichová10.02.2025

Czech National Bank Cuts Interest Rates to 3.75%: What This Means for Your Savings, Mortgages, and Investments

Ondřej Marek29.09.2024

Mortgages and Interest Rates: Why Are They More Expensive Than Everyone Expected?

Ondřej Marek28.05.2024

Early Mortgage Repayment Will Get More Expensive – Limiting “Mortgage Tourism”

Ing. Lukáš Cinko16.04.2024

Options for Reducing Your Mortgage Interest Rate During the Fixed Period

Ing. Alena Lodlová07.12.2023

Major Updates and Changes in 2024 in Building Savings, Mortgages, Insurance, and Pension Savings

Ondřej Marek10.02.2025

Czech National Bank Cuts Interest Rates to 3.75%: What This Means for Your Savings, Mortgages, and Investments

Ondřej Marek07.12.2023