Blog: finance and real estate made simple

Articles and insights to help you navigate and grow

How to Outperform Savings Accounts and Fight Inflation

HISTORY

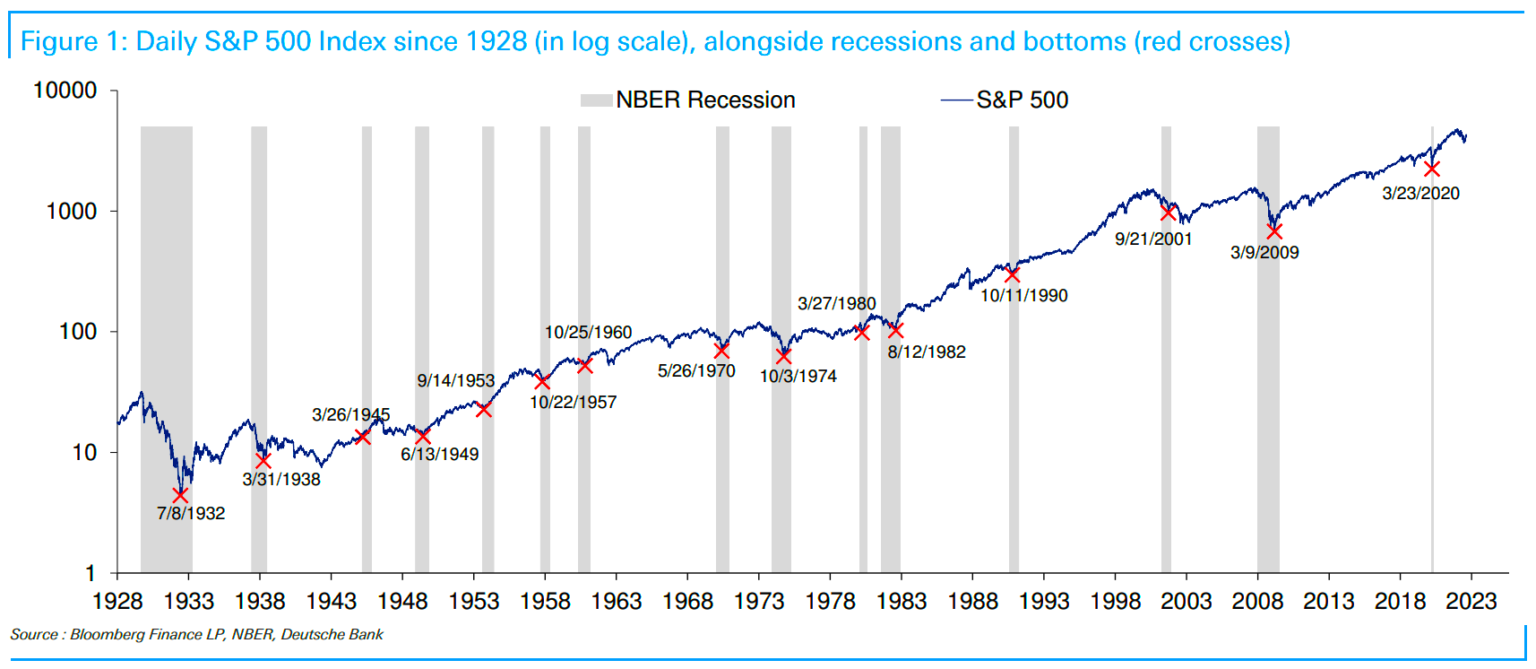

1929, 1937, 1962, 1987, 1990, 2000, 2008, 2020, ????

Do these numbers ring a bell? They represent the years of the biggest stock market crashes over the past nearly 100 years.

Source: Bloomberg Finance LP, NBER, Deutsche Bank

By definition, these are usually very significant drops in stock prices—often tens of percent—and typically happen very quickly. Stocks can crash within hours, days, or at most weeks.

Recovery from such crashes can take several years.

Stock market crashes often follow long periods of growth, when stock prices reach absurd levels.

Crashes are often preceded by unsupported economic growth, extreme debt, heavy use of leverage, war, natural disasters, irresponsible political decisions, etc.

Statistically, stock market crashes occur roughly every 10 years.

Does this sound familiar?

PRESENT

It’s been 14 years since the biggest modern-era crash in 2008. Statistically, another one should be due. Given the factors mentioned above, which can cause downturns, similarities are noticeable.

But nothing like that has happened yet. Why?

Politicians and central banks have learned that they can intervene quickly during crises. Unfortunately, this often comes at the cost of high debt or today’s high inflation.

From a stock perspective, we are currently more in a bear market—meaning prices are slowly but steadily falling due to various factors: war, the energy crisis, high inflation, higher interest rates, risk of recession, and economic instability. These are the reasons why stocks have been losing value this year.

FUTURE

Stocks are generally a good indicator of future events. The changes in the global economy have been apparent since the beginning of 2022.

-

The basket of 500 largest U.S. companies (S&P 500) has declined -17% from the start of the year to November 2022.

-

A basket of nearly 3,000 companies worldwide (MSCI ACWI) fell -14% over the same period.

Are you ready? We can go even further.

We cannot know if the next stock market crash is around the corner. However, there is more uncertainty and negative news today than positive. Why is this still good news for long-term investors? Because the greater the drop, the greater the potential for future growth. In other words, you can currently buy shares of the world’s largest companies at significantly lower prices.

Whatever happens next, the current decline of around 15% is already interesting for long-term and ideally regular investing.

Therefore, I see stocks today as an opportunity for the next decade. We also see a very interesting opportunity in bonds. Due to rising interest rates worldwide, bond prices have dropped significantly. However, the rule is simple: when bond prices fall, future yields increase. Right now is the time to lock in very attractive yields on both corporate and safe government bonds.

Additionally, if we expect that interest rate hikes have peaked (Czech Republic) or are near their peak (USA), we can also anticipate gradual reductions, which will again increase bond prices.

This represents an opportunity that hasn’t existed for many years and is becoming very attractive again.

WHAT DOES THIS MEAN FOR YOU?

If your savings are in a savings account, don’t wait for the “right moment” when stocks hit rock bottom or interest rates drop. By that time, bond and stock prices have usually already risen, and you’ll miss the best growth period. We currently see this as a very interesting time for building a portfolio.

If you already have an investment portfolio, we can review it together to ensure it is structured correctly and aligned with your goals and current market conditions.

Remember, investing doesn’t require much. Usually, all you need is time, patience, and the right partner. If you are interested in a consultation, click the form below and leave your contact details. I will get in touch with you.

Stone & belter blog

Similar articles

Category

11.09.2025

The False Sense of Security Among Entrepreneurs: Financial Advisor? Thanks, I Don’t Need One… Or Do I?

Ing. Marek Jůzl, EFP

11.06.2025

Trump’s Tariffs Shake the Markets: What Does This Mean for Your Investments?

Mgr. Michal Pekař

10.02.2025

Czech National Bank Cuts Interest Rates to 3.75%: What This Means for Your Savings, Mortgages, and Investments

Ondřej Marek

11.09.2025

The False Sense of Security Among Entrepreneurs: Financial Advisor? Thanks, I Don’t Need One… Or Do I?

Ing. Marek Jůzl, EFP11.06.2025

Trump’s Tariffs Shake the Markets: What Does This Mean for Your Investments?

Mgr. Michal Pekař10.02.2025

Czech National Bank Cuts Interest Rates to 3.75%: What This Means for Your Savings, Mortgages, and Investments

Ondřej Marek10.02.2025

Czech National Bank Cuts Interest Rates to 3.75%: What This Means for Your Savings, Mortgages, and Investments

Ondřej Marek