Blog: finance and real estate made simple

Articles and insights to help you navigate and grow

Retirement Around the Corner: Will Your Savings Last a Lifetime?

For some, retirement is still several years away. For others, it’s only a few months. Either way, the time for taking stock is approaching. Are you counting on a state pension, or have you mainly relied on yourself and built your own retirement savings? And that raises the key question: will your savings truly last for the rest of your life?

Before I go into more detail, let me clarify that this is a model scenario.

For better comparison, the examples use an average return of 8% p.a. Such performance is realistic mainly for clients who keep their capital invested long-term even during retirement and withdraw only minimally, or who have other income sources (e.g., business income, company ownership stakes, dividends, or a state pension). However, if we are planning a regular income and gradual portfolio drawdown, it is more reasonable to assume a more conservative return of around 4–5% p.a.

Markets behave differently and future performance cannot be predicted. Every situation is individual. With shorter horizons, part of the portfolio typically becomes more conservative, so it is not realistic to assume a constant 8% long-term return.

Let’s look at several model situations

- Retirement is approaching and today I have a solid amount saved, for example CZK 10,000,000. The question running through my mind: How long will it last? Will it be enough for the rest of my life?

- Or I plan to retire in 10 or 20 years. How long will it take me to accumulate CZK 10,000,000?

- Or I have CZK 2,000,000 today — what will it be worth by the time I retire?

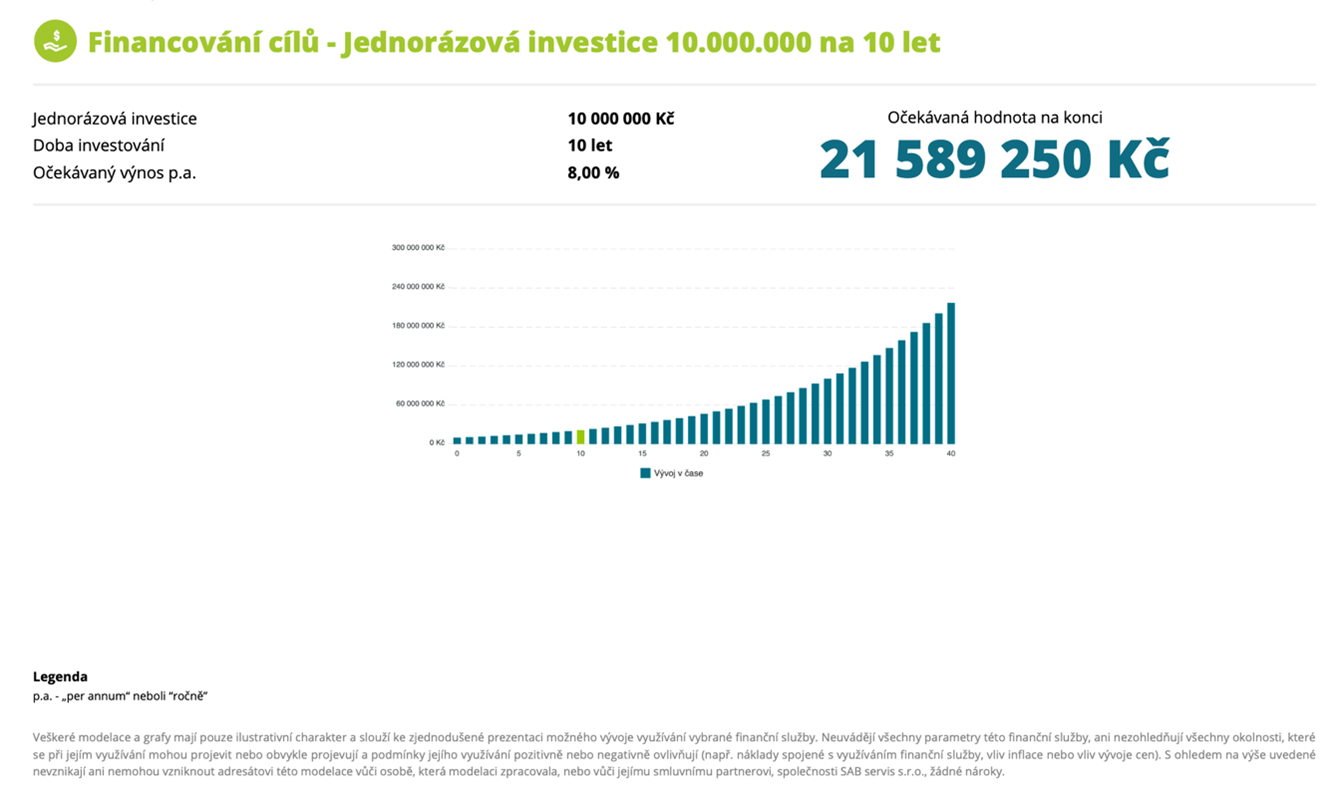

1) CZK 10,000,000 and retirement in 10 years

We invest the original CZK 10,000,000 at 8% annually.

Value after 10 years:

10,000,000 × 1.08¹⁰ ≈ CZK 21,589,000

After 10 years, you could enter the income phase with approximately CZK 21.6 million.

How long would this cover your living expenses?

Let’s assume withdrawals of CZK 70,000 per month = CZK 840,000 per year.

During retirement, the portfolio continues earning an average 8% annually. Markets fluctuate, but the long-term average is around 8%.

Annual return:

8% of 21.6 million ≈ CZK 1,727,000

You withdraw only CZK 840,000, meaning the withdrawal rate is about 3.9%, well below portfolio growth.

What does this mean?

With this withdrawal level, the capital would never be depleted.

On the contrary, it would continue growing. Effectively, this creates an unlimited retirement income. If nothing changes, the portfolio would grow even after withdrawals:

(21.6 million – 840 thousand) + 8% ≈ CZK 22.5 million after the first year, continuing upward in subsequent years.

In this scenario, the income is very secure.

2) CZK 10,000,000 and retiring today

If you have “only” CZK 10,000,000, there is no accumulation period. You start withdrawing immediately: CZK 70,000 per month, assuming 8% annual return.

Initial capital: CZK 10,000,000

Withdrawal: CZK 70,000 per month

Return: 8% p.a. ≈ CZK 800,000 per year

What happens in practice?

You begin withdrawing immediately. Monthly withdrawals gradually reduce the capital, and eventually it will be depleted.

However, this would happen only after approximately 458 months, or about 38 years — an impressively long time.

If withdrawals increased to CZK 90,000 per month, the capital would last roughly 25–30 years.

If reduced to CZK 50,000 per month, withdrawals could be practically unlimited, leaving the remainder to heirs. After all, coffins don’t have pockets.

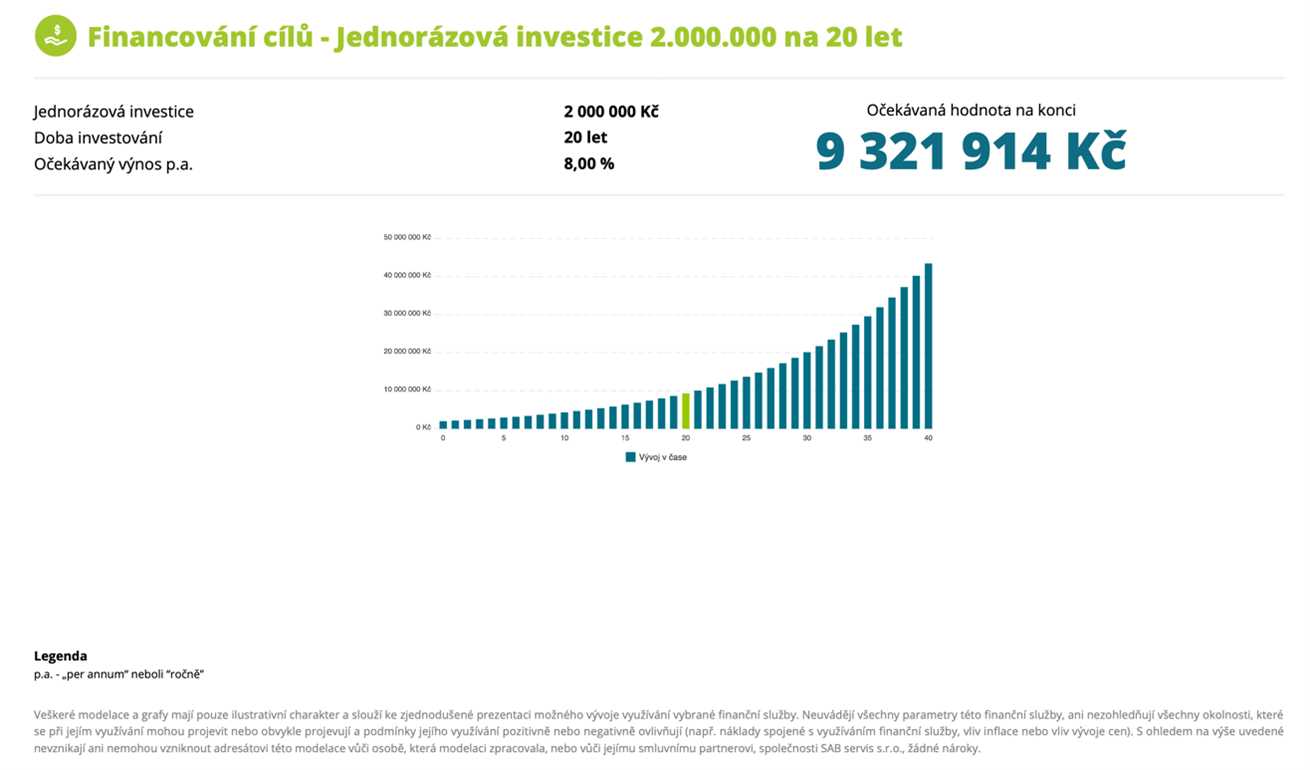

3) CZK 2,000,000 and retirement far away

How much would you need to invest monthly to reach CZK 10,000,000? Again, assuming 8% p.a.

Starting amount: CZK 2,000,000

Target: CZK 10,000,000

Return: 8% p.a. → CZK 9,321,914 after 20 years

The market alone would grow your 2 million to nearly the full target. The remaining amount to save:

10,000,000 – 9,321,000 = CZK 679,000

Required monthly investment?

Approximately CZK 300–320 per month.

With CZK 2,000,000 invested for 20 years at 8%, compound interest does almost all the work.

However, investing only CZK 300 per month may be a missed opportunity. If you have stable income and clear household or business cash flow, I recommend allocating 30% of your income or invoicing toward long-term wealth building.

With CZK 5,000–10,000 per month, you create a solid financial cushion. You may also benefit from DIP, state support, and tax deductions.

Do you know your monthly cash flow? That’s a topic for another article.

For individual planning, contact your advisor.

Kalkulačka

Calculate

-

Monthly rent

Next step with Stone & belter

Get advice and start now!

Stone & belter blog

Similar articles

Category

09.12.2025

DIP Through the Eyes of a Business Owner: Where the Real Tax Savings Lie in 2025

Ing. Marek Jůzl, EFP

08.12.2025

Don’t leave money on the table — claim your 2025 retirement tax deductions

Tomáš Seidel MBA

11.09.2025

The False Sense of Security Among Entrepreneurs: Financial Advisor? Thanks, I Don’t Need One… Or Do I?

Ing. Marek Jůzl, EFP09.12.2025

DIP Through the Eyes of a Business Owner: Where the Real Tax Savings Lie in 2025

Ing. Marek Jůzl, EFP08.12.2025

Don’t leave money on the table — claim your 2025 retirement tax deductions

Tomáš Seidel MBA11.09.2025

The False Sense of Security Among Entrepreneurs: Financial Advisor? Thanks, I Don’t Need One… Or Do I?

Ing. Marek Jůzl, EFP